Market Monitor April 28 ( Alphabet, Nvidia & Meta UP, Intel DOWN)

By Kristoff De Turck - reviewed by Aldwin Keppens

Last update: Apr 28, 2025

US Markets Rise as Big Tech Shines, Trade Tensions Remain a Concern

Strong Finish to a Volatile Week

US stocks ended higher on Friday after a volatile trading session, driven by strength in Big Tech and optimism around key earnings results.

The Nasdaq outperformed, gaining 1.3%, while the S&P 500 added 0.7%. The Dow Jones Industrial Average closed nearly flat, up less than 0.1%.

Alphabet Leads Big Tech Rally

Alphabet (GOOGL | +1.68%) led the charge, jumping 1.5% after delivering better-than-expected first-quarter results.

Strong ad revenue helped push Google's services operating margin up by 300 basis points. The company also announced a massive $70 billion share buyback, further boosting investor sentiment.

JPMorgan praised Google's integration of its AI model, Gemini, into the search engine via "AI Mode," maintaining a Buy rating and raising the price target to $195, implying almost 21% upside.

Other tech heavyweights, including Nvidia (NVDA | +4.3%), Meta (META | +2.65%), and Amazon (AMZN | +1.31%), also gained ground ahead of their own earnings reports next week.

Tesla (TSLA | +9.8%) soared nearly 10% after the US government announced new regulations supporting innovation and commercial deployment of self-driving cars.

Corporate Moves: Spotify, DoorDash, and Intel

Spotify (SPOT | +2.44%) also made headlines, jumping more than 2% after reports it plans to raise subscription prices across dozens of countries, excluding the US.

Meanwhile, DoorDash (DASH | +0.29%) shares edged higher amid news it made a $3.6 billion takeover offer for British food delivery rival Deliveroo. Deliveroo's US-listed shares surged nearly 23% on the announcement.

Not all tech stories were positive. Intel (INTC | -6.7%) fell almost 7% after offering a weaker-than-expected revenue forecast for the current quarter.

Although the chipmaker’s last quarterly earnings beat estimates, concerns over slowing foundry growth and rising losses weighed heavily. Analysts at Citi even suggested Intel should consider exiting its foundry business altogether.

Broader Market Trends and Political Developments

Elsewhere, Abbvie (ABBV | +3.15%) climbed 3.2% after raising its full-year outlook despite a dip in profits.

Energy services giant Schlumberger (SLB | -1.17%) slipped 1.2% after missing earnings expectations.

On a broader level, this week's gains marked a clear recovery from early April’s pullback. However, market strategists like Sam Stovall of CFRA Research cautioned that the S&P 500 hasn't officially exited correction territory until it surpasses its previous February highs.

Political developments also played a role in market sentiment. President Donald Trump indicated he would not remove Federal Reserve Chair Jerome Powell, easing some concerns about political interference. Yet Trump's continued pressure on the Fed could ironically make interest rate cuts less likely, as the central bank seeks to assert its independence.

Trade Tensions Still in Focus

Meanwhile, trade tensions between the US and China remain elevated. Trump reiterated his support for maintaining steep tariffs, calling it a "total victory" if 50% import duties persist into next year.

Negotiations between Washington and Beijing were reportedly ongoing, though Chinese officials denied any active talks were underway.

Economic Outlook and Key Data Ahead

Economic data showed consumer sentiment slipping in April, according to the University of Michigan survey, while inflation expectations climbed sharply, largely due to growing concerns over the trade war.

Looking ahead, investors are bracing for a sharp slowdown in US GDP growth, with expectations of just 0.4% expansion in the first quarter, down from 2.4% in Q4 2024.

In other markets, the 10-year US Treasury yield edged below 4.30%, the euro weakened slightly to 1.1375 against the dollar, and oil prices staged a mild recovery after early losses.

Looking Ahead

As earnings season heats up and geopolitical tensions linger, traders should brace for continued volatility heading into next week.

Daily Market Analysis – April 25, 2025 (After Market Close)

Short Term Trend

- Short-Term Trend: Neutral (no change)

- Support at $500

- Resistance at $550

- Volume: Below average (50)

- Pattern: Follow Through Day, the breakdown's earlier resistance level was regained.

- Short-Term Trend: Neutral (no change)

- Support at $415

- Resistance at $466

- Volume: Below average (50)

- Pattern: Follow Through Day, the breakdown's earlier resistance level was regained.

- Short-Term Trend: Neutral (no change)

- Support at $170

- Resistance at $197

- Volume: Below average (50)

- Pattern: Inside Day, close to resistance

Long Term Trend

- Long-Term Trend: Down (no change)

- Weekly Bullish Engulfing candle

- Long-Term Trend: Down (no change)

- Weekly Bullish Engulfing candle

- Long-Term Trend: Down (no change)

- Weekly Bullish Engulfing candle

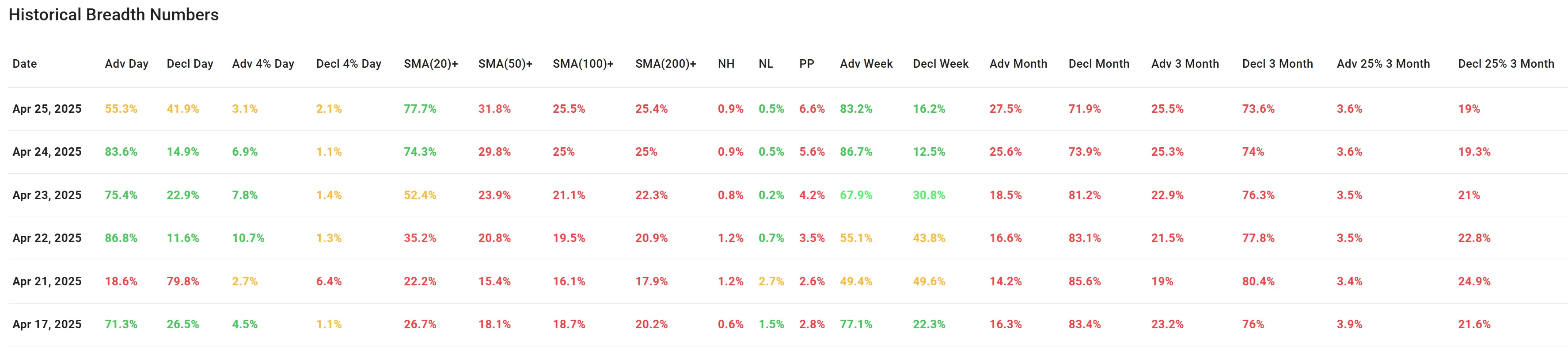

Market Breadth Analysis for April 24, 2025 (After Market Close)

The US market closed the week with mixed but relatively positive breadth data. While the percentage of advancing stocks dipped compared to the previous two sessions, broader participation across key technical levels remains robust.

Daily Advances vs. Declines

April 25, 2025 saw 55.3% of stocks advancing versus 41.9% declining — a noticeable pullback from the prior two days, when over 83% of stocks were advancing.

This slight deterioration follows several strong breadth days (April 22–24), signaling that although momentum remains positive, the market might be entering a digestion phase after the sharp rally earlier in the week.

Compared to April 21, when only 18.6% of stocks advanced, the broader trend has clearly improved.

- Positive: Advance numbers remain above 50%.

- Caution: Slight weakening compared to the peak breadth earlier this week.

Stocks Above Key Moving Averages (SMA)

SMA(20)+ participation improved sharply over the week: from 22.2% on April 21 to 77.7% by April 25.

SMA(50)+ and SMA(100)+ levels remain subdued (around 30% and 25% respectively), indicating that while short-term momentum is strong, medium- to longer-term technical strength is still rebuilding.

SMA(200)+ readings are slowly ticking higher but remain below 30%, suggesting the longer-term technical trend has not yet fully turned bullish.

-

Positive: Short-term technical improvement is strong (SMA(20)+).

-

Caution: Medium- and long-term breadth still needs work.

Weekly and Monthly Breadth

Weekly Advances stayed high at 83.2%, up from 55.1% earlier in the week, confirming a broad-based recovery.

Monthly Advance numbers remain weak (around 27.5%), reinforcing the idea that recent strength is still relatively young compared to the broader downtrend seen earlier this year.

Visual Trends

The first chart shows how daily advances surged midweek, peaking on April 22-24 before cooling slightly.

The second chart illustrates that the percentage of stocks trading above their 20-day moving averages is climbing rapidly, whereas participation above longer-term averages (50-, 100-, and 200-day SMAs) remains lower but is gradually improving.

Conclusion

The market breadth paints a cautiously optimistic picture. After a heavy sell-off earlier in April, breadth has significantly improved over the past week.

The fact that fewer stocks are trading above their 50-day and 200-day moving averages suggests that a sustainable uptrend will require more time and confirmation.

Key Takeaway:

Short-term momentum is positive, but for a true long-term bull trend to take hold, more participation across intermediate- and long-term moving averages is necessary.

EPA:ABBV (8/29/2017, 5:08:56 PM)

58.01

-5.09 (-8.07%)

34.52

-0.41 (-1.17%)

188.99

+2.45 (+1.31%)

163.85

+2.38 (+1.47%)

20.05

-1.44 (-6.7%)

111.01

+4.58 (+4.3%)

284.95

+25.44 (+9.8%)

547.27

+14.12 (+2.65%)

620.72

+14.77 (+2.44%)

187.76

+0.54 (+0.29%)

Find more stocks in the Stock Screener

ABBV.PA Latest News and Analysis

3 hours ago - ChartmillMarket Monitor April 28 ( Alphabet, Nvidia & Meta UP, Intel DOWN)

3 hours ago - ChartmillMarket Monitor April 28 ( Alphabet, Nvidia & Meta UP, Intel DOWN)US Markets Rise as Big Tech Shines, Trade Tensions Remain a Concern