Zoetis (NYSE:ZTS) Posts Q4 Sales In Line With Estimates But Stock Drops

Provided By StockStory

Last update: Feb 13, 2025

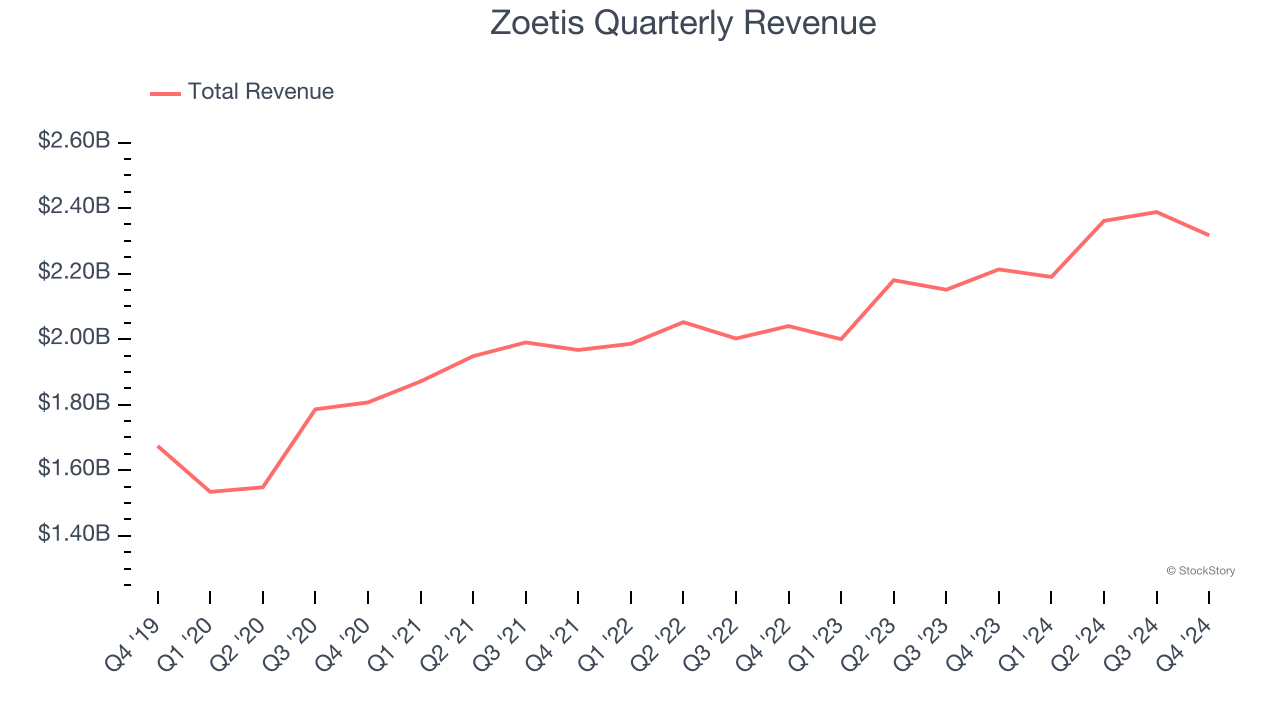

Animal health company Zoetis (NYSE:ZTS) met Wall Street’s revenue expectations in Q4 CY2024, with sales up 4.7% year on year to $2.32 billion. On the other hand, the company’s full-year revenue guidance of $9.3 billion at the midpoint came in 2.8% below analysts’ estimates. Its non-GAAP profit of $1.40 per share was 4.7% above analysts’ consensus estimates.

Is now the time to buy Zoetis? Find out by accessing our full research report, it’s free.

Zoetis (ZTS) Q4 CY2024 Highlights:

- Revenue: $2.32 billion vs analyst estimates of $2.32 billion (4.7% year-on-year growth, in line)

- Adjusted EPS: $1.40 vs analyst estimates of $1.34 (4.7% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $9.3 billion at the midpoint, missing analyst estimates by 2.8% and implying 0.5% growth (vs 8.4% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $6.05 at the midpoint, missing analyst estimates by 3.9%

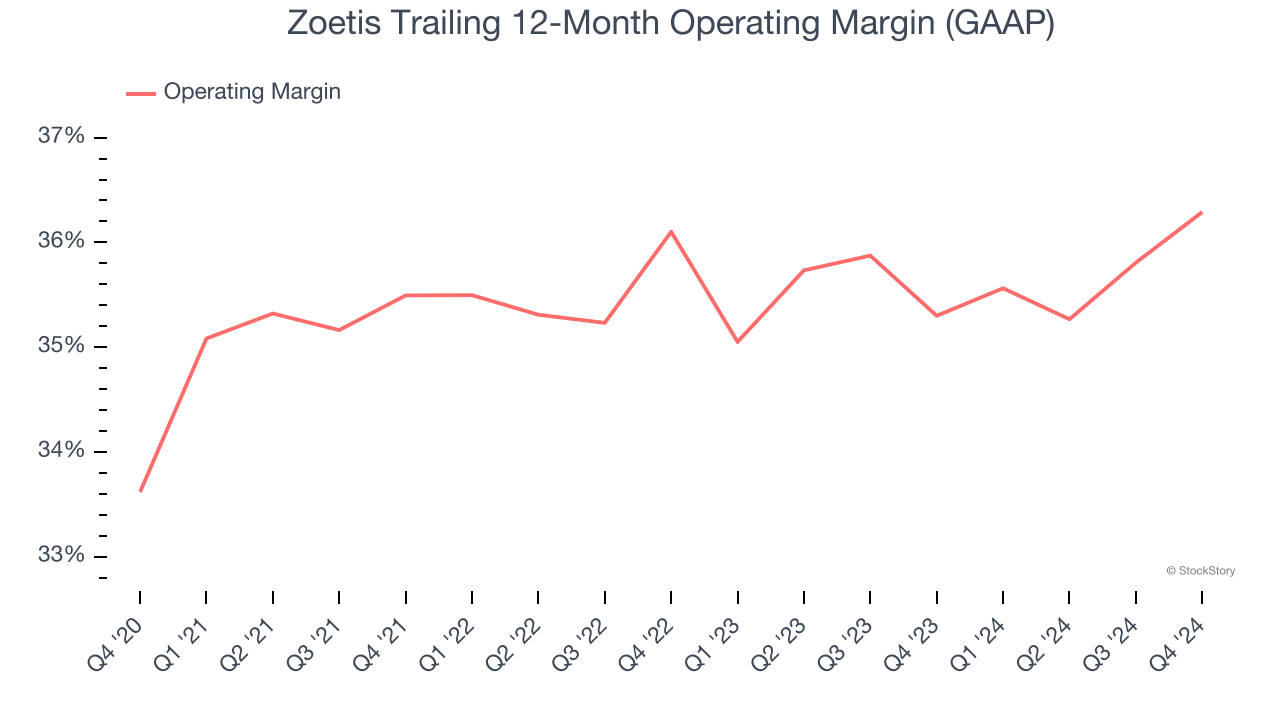

- Operating Margin: 33.8%, up from 31.7% in the same quarter last year

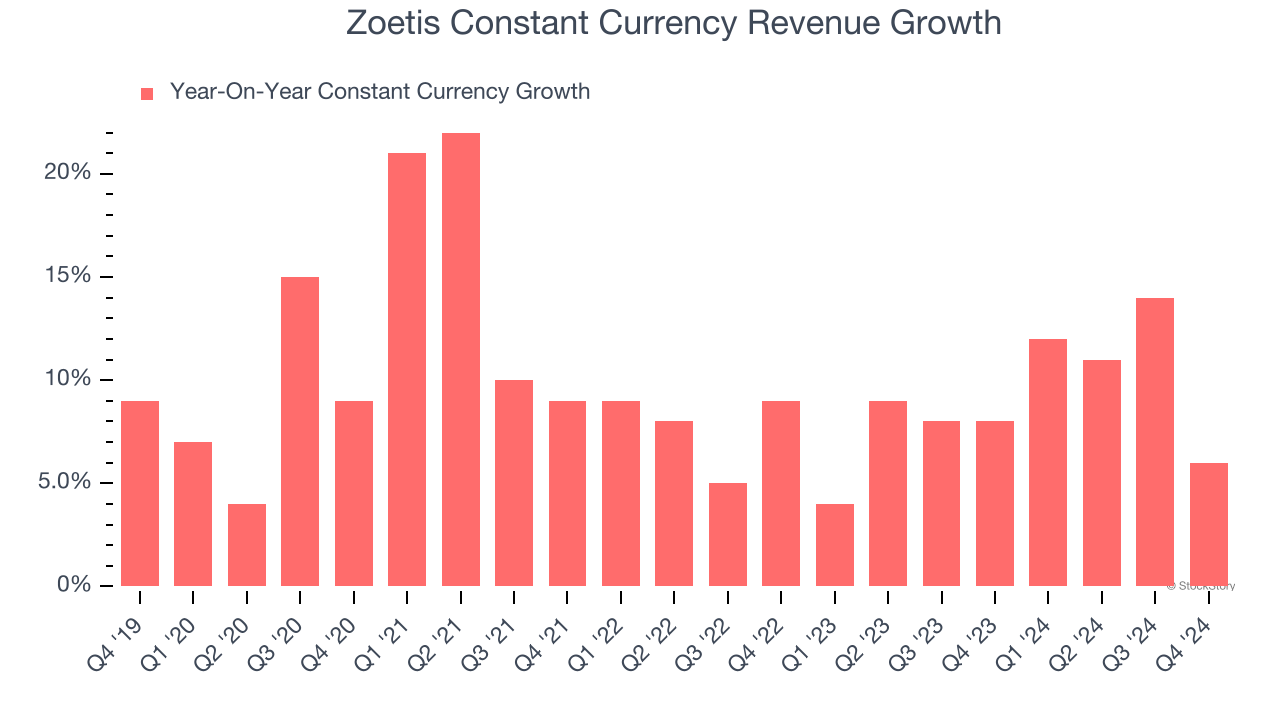

- Constant Currency Revenue rose 6% year on year (8% in the same quarter last year)

- Market Capitalization: $78.45 billion

“Zoetis delivered excellent full year results in 2024, driven by the demand for our innovative products and the strength of our key franchises,” said Kristin Peck, Chief Executive Officer of Zoetis.

Company Overview

Originally a subsidiary of Pfizer, Zoetis (NYSE:ZTS) is an animal health company that develops and distributes medicines, vaccines, and diagnostic products for livestock and pets.

Branded Pharmaceuticals

The branded pharmaceutical industry relies on a high-cost, high-reward business model, driven by substantial investments in research and development to create innovative, patent-protected drugs. Successful products can generate significant revenue streams over their patent life, and the larger a roster of drugs, the stronger a moat a company enjoys. However, the business model is inherently risky, with high failure rates during clinical trials, lengthy regulatory approval processes, and intense competition from generic and biosimilar manufacturers once patents expire. These challenges, combined with scrutiny over drug pricing, create a complex operating environment. Looking ahead, the industry is positioned for tailwinds from advancements in precision medicine, increasing adoption of AI to enhance drug development efficiency, and growing global demand for treatments addressing chronic and rare diseases. However, headwinds include heightened regulatory scrutiny, pricing pressures from governments and insurers, and the looming patent cliffs for key blockbuster drugs. Patent cliffs bring about competition from generics, forcing branded pharmaceutical companies back to the drawing board to find the next big thing.

Sales Growth

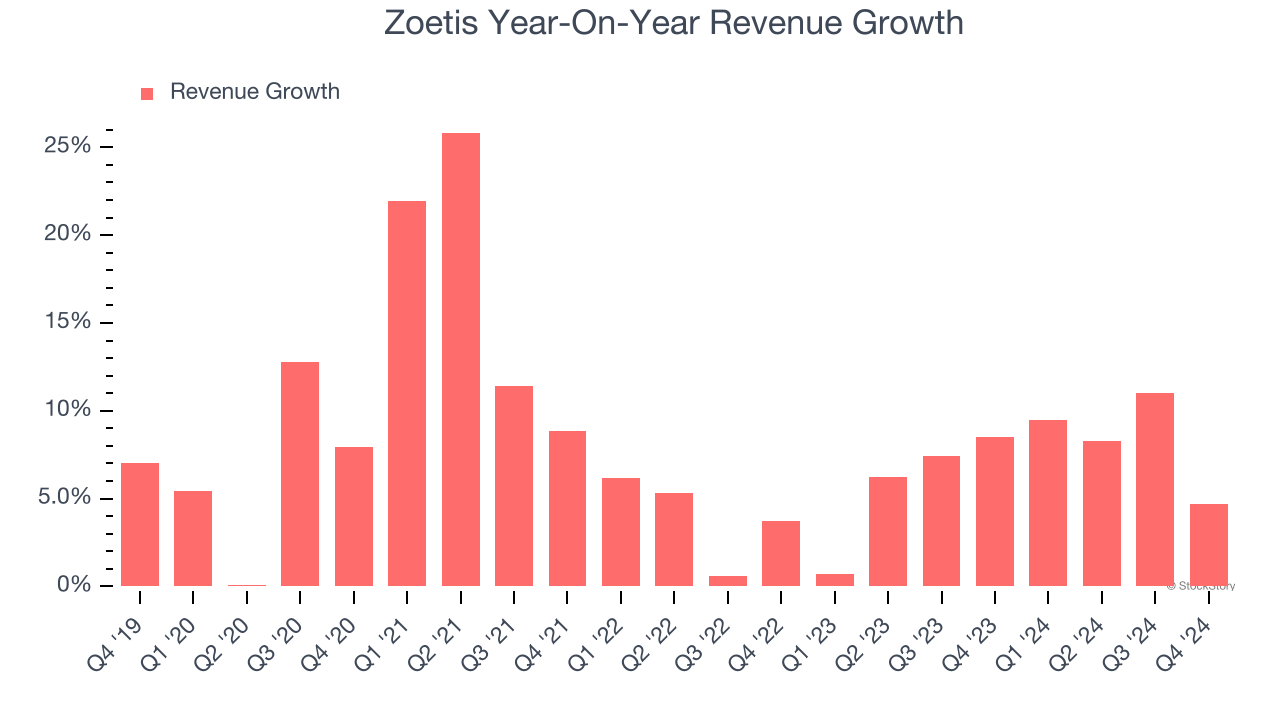

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Zoetis’s sales grew at a decent 8.1% compounded annual growth rate over the last five years. Its growth was slightly above the average healthcare company and shows its offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within healthcare, a half-decade historical view may miss recent innovations or disruptive industry trends. Zoetis’s recent history shows its demand slowed as its annualized revenue growth of 7% over the last two years is below its five-year trend.

We can better understand the company’s sales dynamics by analyzing its constant currency revenue, which excludes currency movements that are outside their control and not indicative of demand. Over the last two years, its constant currency sales averaged 9% year-on-year growth. Because this number is better than its normal revenue growth, we can see that foreign exchange rates have been a headwind for Zoetis.

This quarter, Zoetis grew its revenue by 4.7% year on year, and its $2.32 billion of revenue was in line with Wall Street’s estimates.

Looking ahead, sell-side analysts expect revenue to grow 2.4% over the next 12 months, a deceleration versus the last two years. This projection doesn't excite us and implies its products and services will face some demand challenges. At least the company is tracking well in other measures of financial health.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefiting from the rise of AI, available to you FREE via this link.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after subtracting all core expenses, like marketing and R&D.

Zoetis has been a well-oiled machine over the last five years. It demonstrated elite profitability for a healthcare business, boasting an average operating margin of 35.4%.

Looking at the trend in its profitability, Zoetis’s operating margin rose by 2.7 percentage points over the last five years, as its sales growth gave it operating leverage. This performance was mostly driven by its past improvements as the company’s margin was relatively unchanged on two-year basis.

In Q4, Zoetis generated an operating profit margin of 33.8%, up 2.1 percentage points year on year. This increase was a welcome development and shows it was recently more efficient because its expenses grew slower than its revenue.

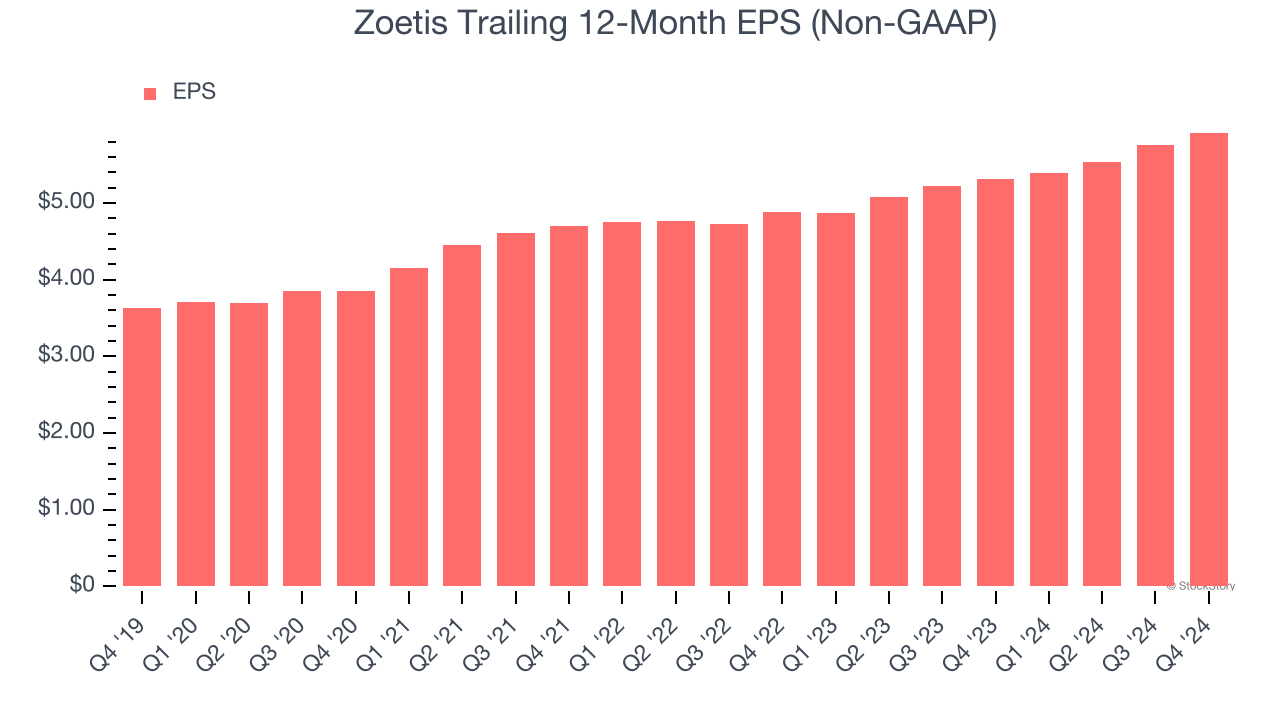

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Zoetis’s EPS grew at a remarkable 10.2% compounded annual growth rate over the last five years, higher than its 8.1% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

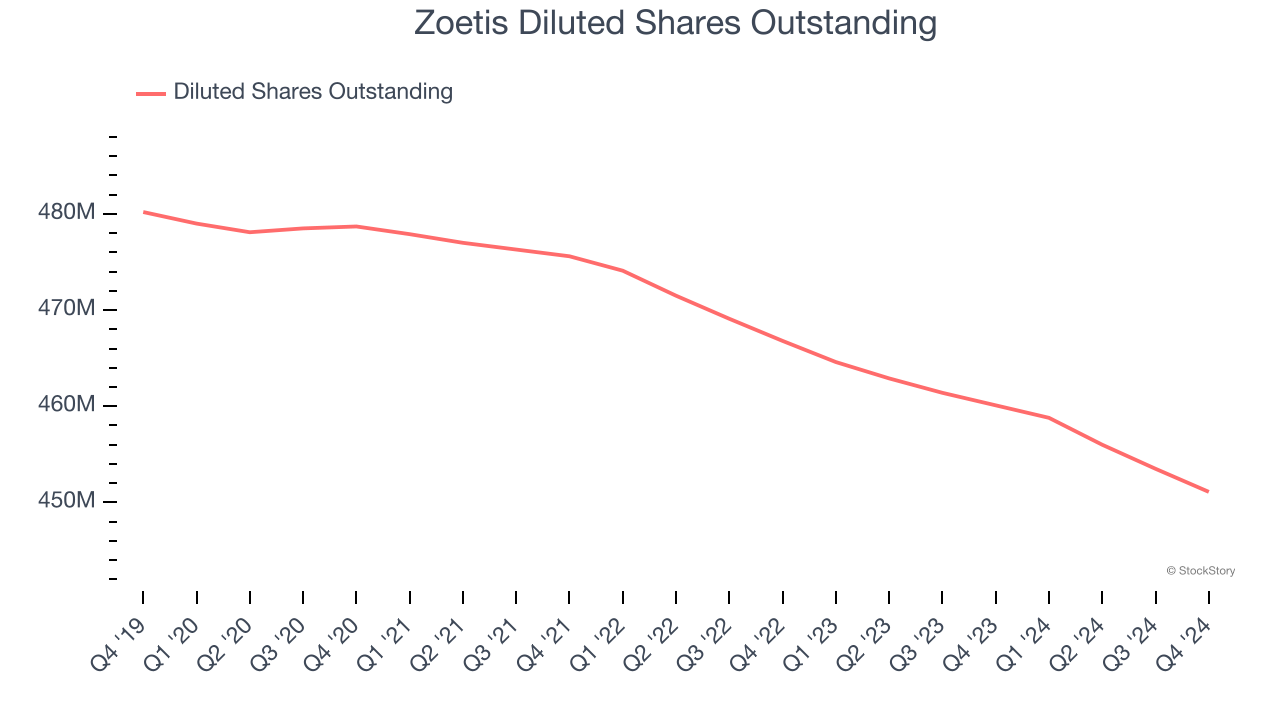

Diving into Zoetis’s quality of earnings can give us a better understanding of its performance. As we mentioned earlier, Zoetis’s operating margin expanded by 2.7 percentage points over the last five years. On top of that, its share count shrank by 6.1%. These are positive signs for shareholders because improving profitability and share buybacks turbocharge EPS growth relative to revenue growth.

In Q4, Zoetis reported EPS at $1.40, up from $1.24 in the same quarter last year. This print beat analysts’ estimates by 4.7%. Over the next 12 months, Wall Street expects Zoetis’s full-year EPS of $5.92 to grow 5.1%.

Key Takeaways from Zoetis’s Q4 Results

We struggled to find many positives in these results. Its full-year EPS guidance missed significantly and its full-year revenue guidance fell short of Wall Street’s estimates. Overall, this was a softer quarter. The stock traded down 9.2% to $157.81 immediately after reporting.

Zoetis underperformed this quarter, but does that create an opportunity to invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.

26.3

+0.4 (+1.54%)

160.46

+3.04 (+1.93%)

Find more stocks in the Stock Screener

PFE Latest News and Analysis

21 hours ago - ChartmillThese S&P500 stocks are the most active in today's session

21 hours ago - ChartmillThese S&P500 stocks are the most active in today's sessionLet's have a look at what is happening on the US markets on Friday. Below you can find the most active S&P500 stocks in today's session.

2 days ago - ChartmillCurious about the most active S&P500 stocks in today's session?Explore the S&P500 index on Thursday and find out which stocks are the most active in today's session. Stay updated with the stocks that are capturing market interest and driving market movements.

3 days ago - ChartmillWhich S&P500 stocks are the most active on Wednesday?Stay informed about the most active stocks in the S&P500 index on Wednesday's session. Discover the stocks that are generating the highest trading volume and driving market activity.

4 days ago - ChartmillWhich S&P500 stocks are the most active on Tuesday?Let's have a look at what is happening on the US markets on Tuesday. Below you can find the most active S&P500 stocks in today's session.

12 days ago - ChartmillExplore the S&P500 index on Monday and find out which stocks are the most active in today's session.Curious about the most active S&P500 stocks in today's session? Join us as we explore the US markets on Monday and uncover the stocks that are leading the way in terms of trading volume and market attention.

16 days ago - ChartmillMost active S&P500 stocks in Thursday's sessionLet's have a look at what is happening on the US markets on Thursday. Below you can find the most active S&P500 stocks in today's session.

18 days ago - ChartmillLooking for the most active stocks in the S&P500 index on Tuesday?Stay informed about the most active S&P500 stocks in today's session as we take a closer look at what's happening on the US markets on Tuesday. Discover the stocks that are generating the highest trading volume and driving market activity.

19 days ago - ChartmillWhich S&P500 stocks are the most active on Monday?Curious about the most active S&P500 stocks in today's session? Get insights into the stocks that are leading the way in terms of trading volume and market attention.