Five9 (NASDAQ:FIVN) Exceeds Q4 Expectations, Stock Soars

Provided By StockStory

Last update: Feb 20, 2025

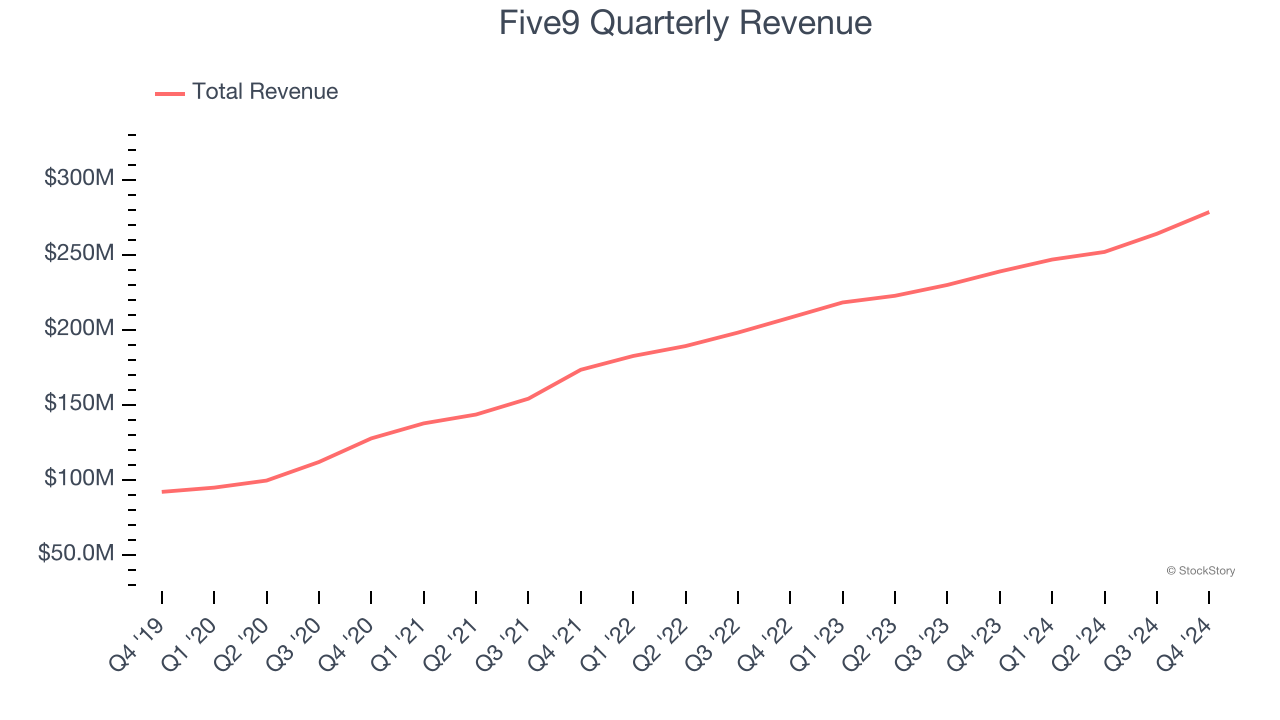

Call center software provider Five9 (NASDAQ: FIVN) beat Wall Street’s revenue expectations in Q4 CY2024, with sales up 16.6% year on year to $278.7 million. The company expects next quarter’s revenue to be around $272 million, close to analysts’ estimates. Its non-GAAP profit of $0.47 per share was 33% below analysts’ consensus estimates.

Is now the time to buy Five9? Find out by accessing our full research report, it’s free.

Five9 (FIVN) Q4 CY2024 Highlights:

- Revenue: $278.7 million vs analyst estimates of $267.9 million (16.6% year-on-year growth, 4% beat)

- Adjusted EBITDA: $64.26 million vs analyst estimates of $55.94 million (23.1% margin, 14.9% beat)

- Management’s revenue guidance for the upcoming financial year 2025 is $1.14 billion at the midpoint, in line with analyst expectations and implying 9.6% growth (vs 14.4% in FY2024)

- Adjusted EPS guidance for the upcoming financial year 2025 is $2.60 at the midpoint, beating analyst estimates by 2.2%

- Operating Margin: 1.5%, up from -7.8% in the same quarter last year

- Free Cash Flow Margin: 11.7%, up from 7.9% in the previous quarter

- Market Capitalization: $3.15 billion

“We are very pleased to report strong year end results, with 2024 annual revenue exceeding $1 billion. Fourth quarter revenue growth accelerated to 17%, driven by our subscription revenue growing 19%. We reached an all-time record adjusted EBITDA margin of 23%, helping drive our highest ever quarterly operating cash flow of $50 million. Throughout the year, we extended our leadership position in AI by further enhancing our AI-powered platform to deliver the New CX. Our record results and strong traction in our AI business continue to demonstrate the power of our platform in enabling brands to elevate their CX in this rapidly evolving world of AI as evidenced by our Enterprise AI revenue growing 46% YoY in the fourth quarter. We believe we are well positioned with our AI-powered platform and trusted AI experts to continue driving durable long-term growth and look forward to building on our momentum in 2025.”

Company Overview

Started in 2001, Five9 (NASDAQ: FIVN) offers software-as-a-service that makes it easier for companies to set up and efficiently run call centers to offer more tailored customer support.

Video Conferencing

Work is becoming more distributed, both across geographies and devices. In order for businesses to keep functioning efficiently, they need to be able to communicate as well as they did when the teams were co-located, which drives the demand for integrated communication platforms.

Sales Growth

Examining a company’s long-term performance can provide clues about its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, Five9 grew its sales at a 19.6% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our benchmark for the software sector, which enjoys a number of secular tailwinds.

This quarter, Five9 reported year-on-year revenue growth of 16.6%, and its $278.7 million of revenue exceeded Wall Street’s estimates by 4%. Company management is currently guiding for a 10.1% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 9.3% over the next 12 months, a deceleration versus the last three years. This projection is underwhelming and indicates its products and services will see some demand headwinds.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Customer Acquisition Efficiency

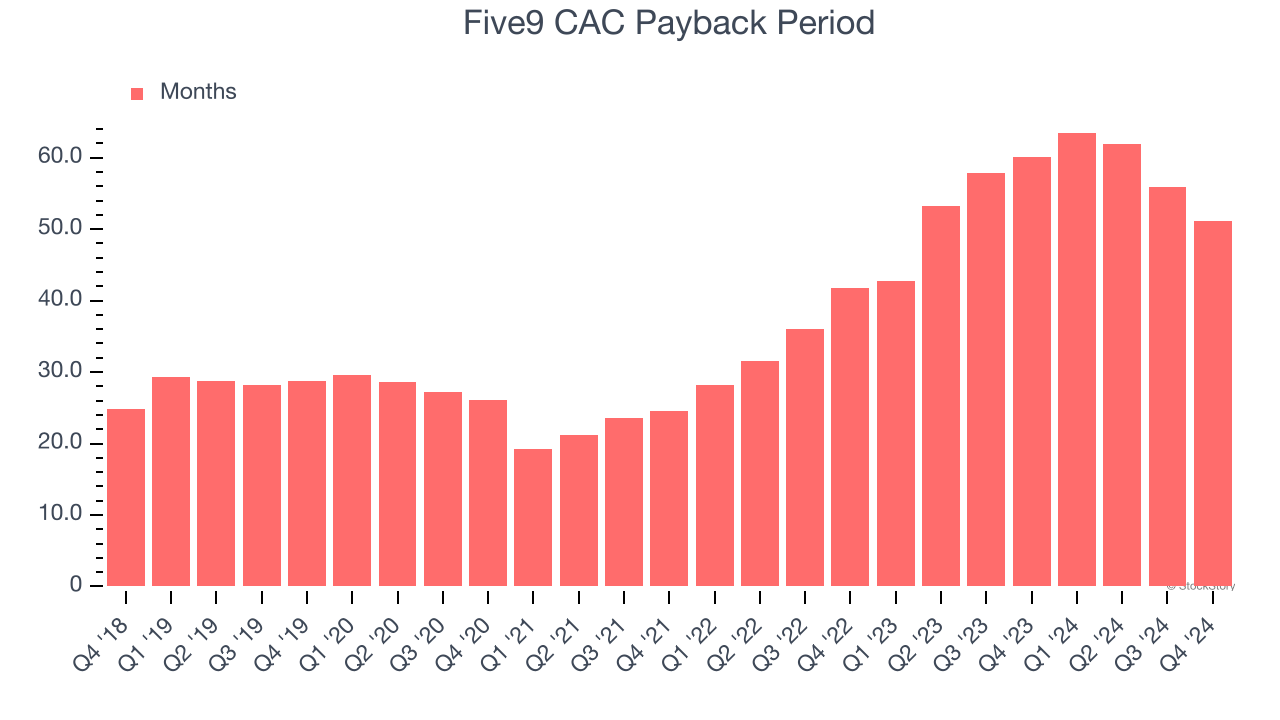

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

It’s relatively expensive for Five9 to acquire new customers as its CAC payback period checked in at 51.2 months this quarter. The company’s slow recovery of its sales and marketing expenses indicates it operates in a highly competitive market and must invest to stand out, even if the return on that investment is low.

Key Takeaways from Five9’s Q4 Results

We were impressed by how significantly Five9 blew past analysts’ EBITDA expectations this quarter. We were also glad its full-year EPS guidance exceeded Wall Street’s estimates. On the other hand, its revenue guidance for next year suggests a significant slowdown in demand. Overall, we think this was still a solid quarter with some key areas of upside. The stock traded up 9.2% to $45.68 immediately following the results.

Five9 put up rock-solid earnings, but one quarter doesn’t necessarily make the stock a buy. Let’s see if this is a good investment. The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free.