Why NYSE:WST qualifies as a good dividend investing stock.

By Mill Chart

Last update: Nov 28, 2024

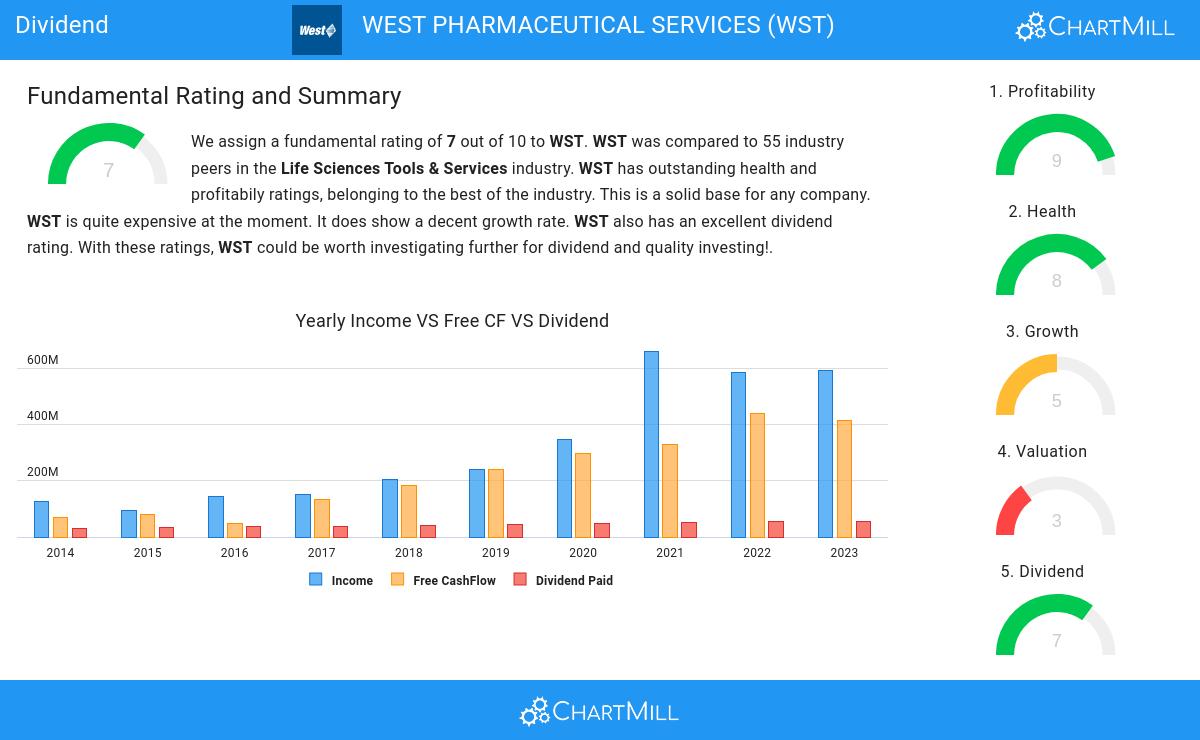

Our stock screener has singled out WEST PHARMACEUTICAL SERVICES (NYSE:WST) as a promising choice for dividend investors. NYSE:WST not only scores well in profitability, solvency, and liquidity but also offers a decent dividend. We'll explore this further.

Understanding NYSE:WST's Dividend

An integral part of ChartMill's stock analysis is the Dividend Rating, which spans from 0 to 10. This rating evaluates diverse dividend factors, including yield, historical data, growth, and sustainability. NYSE:WST has received a 7 out of 10:

- WST's Dividend Yield is rather good when compared to the industry average which is at 0.68. WST pays more dividend than 85.45% of the companies in the same industry.

- The dividend of WST is nicely growing with an annual growth rate of 6.31%!

- WST has been paying a dividend for at least 10 years, so it has a reliable track record.

- WST has not decreased its dividend for at least 10 years, so it has a reliable track record of non decreasing dividend.

- 11.73% of the earnings are spent on dividend by WST. This is a low number and sustainable payout ratio.

- The dividend of WST is growing, but earnings are growing more, so the dividend growth is sustainable.

Understanding NYSE:WST's Health Score

ChartMill employs its own Health Rating for stock assessment. This rating, ranging from 0 to 10, is calculated by examining various liquidity and solvency ratios. In the case of NYSE:WST, the assigned 8 reflects its health status:

- An Altman-Z score of 18.34 indicates that WST is not in any danger for bankruptcy at the moment.

- With an excellent Altman-Z score value of 18.34, WST belongs to the best of the industry, outperforming 100.00% of the companies in the same industry.

- The Debt to FCF ratio of WST is 0.64, which is an excellent value as it means it would take WST, only 0.64 years of fcf income to pay off all of its debts.

- With an excellent Debt to FCF ratio value of 0.64, WST belongs to the best of the industry, outperforming 90.91% of the companies in the same industry.

- A Debt/Equity ratio of 0.07 indicates that WST is not too dependend on debt financing.

- WST has a Debt to Equity ratio of 0.07. This is in the better half of the industry: WST outperforms 63.64% of its industry peers.

- WST has a Current Ratio of 3.00. This indicates that WST is financially healthy and has no problem in meeting its short term obligations.

- A Quick Ratio of 2.23 indicates that WST has no problem at all paying its short term obligations.

A Closer Look at Profitability for NYSE:WST

ChartMill employs its own Profitability Rating system for stock evaluation. This score, ranging from 0 to 10, is derived from an analysis of diverse profitability metrics and margins. In the case of NYSE:WST, the assigned 9 is noteworthy for profitability:

- WST has a better Return On Assets (13.59%) than 94.55% of its industry peers.

- WST has a Return On Equity of 18.15%. This is amongst the best in the industry. WST outperforms 92.73% of its industry peers.

- WST's Return On Invested Capital of 15.28% is amongst the best of the industry. WST outperforms 94.55% of its industry peers.

- WST had an Average Return On Invested Capital over the past 3 years of 20.47%. This is significantly above the industry average of 10.44%.

- The last Return On Invested Capital (15.28%) for WST is well below the 3 year average (20.47%), which needs to be investigated, but indicates that WST had better years and this may not be a problem.

- The Profit Margin of WST (17.37%) is better than 90.91% of its industry peers.

- In the last couple of years the Profit Margin of WST has grown nicely.

- The Operating Margin of WST (20.37%) is better than 87.27% of its industry peers.

- WST's Operating Margin has improved in the last couple of years.

- In the last couple of years the Gross Margin of WST has grown nicely.

Every day, new Best Dividend stocks can be found on ChartMill in our Best Dividend screener.

Check the latest full fundamental report of WST for a complete fundamental analysis.

Keep in mind

This is not investing advice! The article highlights some of the observations at the time of writing, but you should always make your own analysis and invest based on your own insights.

201.9

-7.23 (-3.46%)

Find more stocks in the Stock Screener

WST Latest News and Analysis

12 hours ago - ChartmillWhat's going on in today's session: S&P500 movers

12 hours ago - ChartmillWhat's going on in today's session: S&P500 moversStay updated with the movement of S&P500 stocks in today's session. Discover which S&P500 stocks are making waves on Thursday.

14 hours ago - ChartmillThese S&P500 stocks are gapping in today's session

14 hours ago - ChartmillThese S&P500 stocks are gapping in today's sessionStay tuned for the market movements in the S&P500 index on Thursday. Check out the gap up and gap down stocks in the S&P500 index during today's session.

16 hours ago - ChartmillTop S&P500 movers in Thursday's pre-market session

16 hours ago - ChartmillTop S&P500 movers in Thursday's pre-market sessionLet's have a look at what is happening on the US markets before the opening bell on Thursday. Below you can find the top S&P500 gainers and losers in today's pre-market session.

9 days ago - ChartmillStay updated with the S&P500 stocks that are on the move in today's pre-market session.Before the opening bell on Wednesday, let's take a glimpse of the US markets and explore the S&P500 top gainers and losers in today's pre-market session.

10 days ago - ChartmillWhich S&P500 stocks are gapping on Tuesday?Curious about the market action on Tuesday? Dive into the US markets to explore the gap up and gap down stocks in the S&P500 index during today's session.