Is NYSE:STLA a Good Fit for Dividend Investing?

By Mill Chart

Last update: Sep 25, 2024

STELLANTIS NV (NYSE:STLA) was identified as a stock worth exploring by dividend investors by our stock screener. NYSE:STLA scores well on profitability, solvency and liquidity. At the same time it seems to pay a decent dividend. We'll explore this a bit deeper below.

Deciphering NYSE:STLA's Dividend Rating

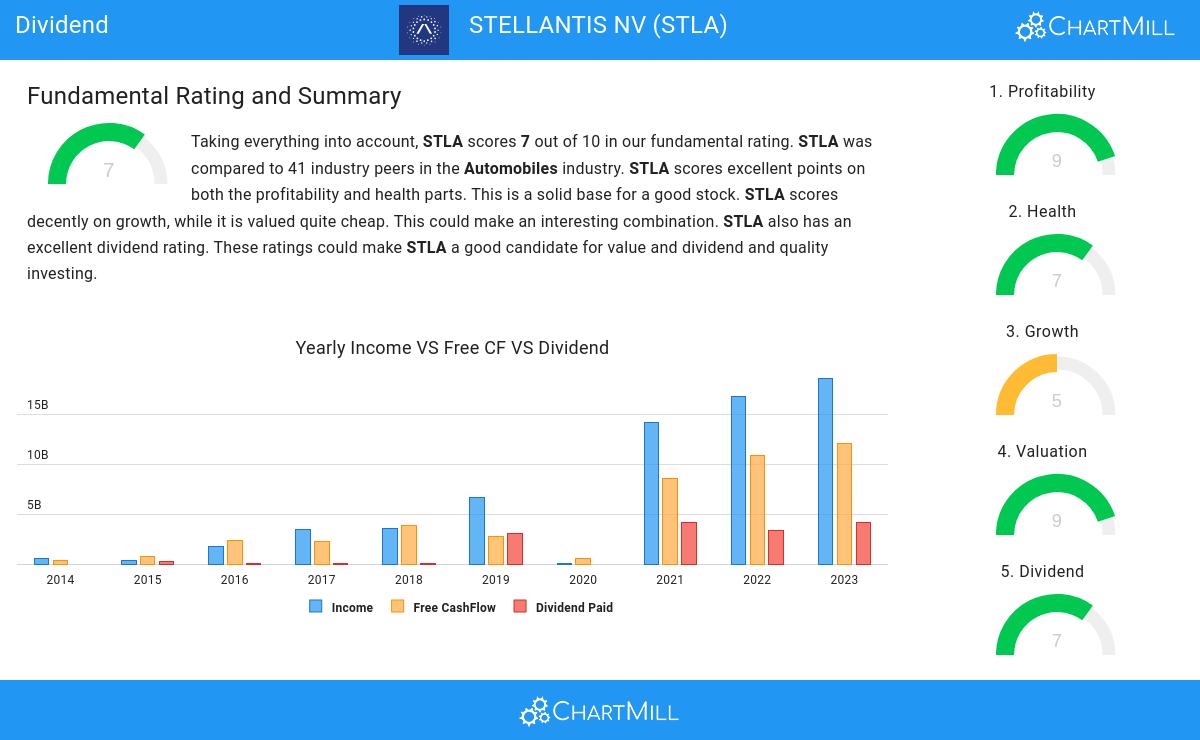

An integral part of ChartMill's stock analysis is the Dividend Rating, which spans from 0 to 10. This rating evaluates diverse dividend factors, including yield, historical data, growth, and sustainability. NYSE:STLA has received a 7 out of 10:

- STLA has a Yearly Dividend Yield of 11.11%, which is a nice return.

- STLA's Dividend Yield is rather good when compared to the industry average which is at 3.47. STLA pays more dividend than 100.00% of the companies in the same industry.

- STLA's Dividend Yield is rather good when compared to the S&P500 average which is at 2.21.

- The dividend of STLA is nicely growing with an annual growth rate of 386.64%!

- STLA has been paying a dividend for over 5 years, so it has already some track record.

- 22.63% of the earnings are spent on dividend by STLA. This is a low number and sustainable payout ratio.

Analyzing Health Metrics

ChartMill utilizes a Health Rating to assess stocks, scoring them on a scale of 0 to 10. This rating takes into account a variety of liquidity and solvency ratios, both in absolute terms and in comparison to industry peers. NYSE:STLA has earned a 7 out of 10:

- Looking at the Altman-Z score, with a value of 2.18, STLA belongs to the top of the industry, outperforming 82.93% of the companies in the same industry.

- The Debt to FCF ratio of STLA is 2.43, which is a good value as it means it would take STLA, 2.43 years of fcf income to pay off all of its debts.

- STLA has a Debt to FCF ratio of 2.43. This is amongst the best in the industry. STLA outperforms 97.56% of its industry peers.

- A Debt/Equity ratio of 0.24 indicates that STLA is not too dependend on debt financing.

- STLA does not score too well on the current and quick ratio evaluation. However, as it has excellent solvency and profitability, these ratios do not necessarly indicate liquidity issues and need to be evaluated against the specifics of the business.

Profitability Insights: NYSE:STLA

ChartMill employs its own Profitability Rating system for stock evaluation. This score, ranging from 0 to 10, is derived from an analysis of diverse profitability metrics and margins. In the case of NYSE:STLA, the assigned 9 is noteworthy for profitability:

- STLA has a better Return On Assets (9.20%) than 92.68% of its industry peers.

- STLA's Return On Equity of 22.76% is amongst the best of the industry. STLA outperforms 92.68% of its industry peers.

- STLA has a better Return On Invested Capital (15.22%) than 95.12% of its industry peers.

- The Average Return On Invested Capital over the past 3 years for STLA is above the industry average of 10.91%.

- The 3 year average ROIC (14.80%) for STLA is below the current ROIC(15.22%), indicating increased profibility in the last year.

- STLA has a Profit Margin of 9.81%. This is amongst the best in the industry. STLA outperforms 87.80% of its industry peers.

- In the last couple of years the Profit Margin of STLA has grown nicely.

- STLA's Operating Margin of 12.19% is amongst the best of the industry. STLA outperforms 95.12% of its industry peers.

- STLA's Operating Margin has improved in the last couple of years.

- STLA's Gross Margin of 20.12% is fine compared to the rest of the industry. STLA outperforms 73.17% of its industry peers.

- In the last couple of years the Gross Margin of STLA has grown nicely.

More Best Dividend stocks can be found in our Best Dividend screener.

Our latest full fundamental report of STLA contains the most current fundamental analsysis.

Keep in mind

This article should in no way be interpreted as advice. The article is based on the observed metrics at the time of writing, but you should always make your own analysis and trade or invest at your own responsibility.

NYSE:STLA (4/28/2025, 2:03:59 PM)

9.345

-0.07 (-0.8%)

Find more stocks in the Stock Screener

STLA Latest News and Analysis

14 days ago - ChartmillMarket Monitor April 15 Before Market Open ( Dell, Palantir UP, Meta DOWN)

14 days ago - ChartmillMarket Monitor April 15 Before Market Open ( Dell, Palantir UP, Meta DOWN)Wall Street Starts Easter Week Strong as Tariff Concerns Ease

18 days ago - ChartmillExploring STELLANTIS NV (NYSE:STLA)'s dividend characteristics.

18 days ago - ChartmillExploring STELLANTIS NV (NYSE:STLA)'s dividend characteristics.Is STELLANTIS NV (NYSE:STLA) a Good Fit for Dividend Investing?