Within 0.2% of its January all-time high. That's where the S&P 500 closed on Tuesday, not quite there yet, but close enough that the question investors are asking has quietly shifted from "when does this market stabilize?" to "when does it print a new record?"

The Rundown

- Peace talks between the US and Iran showed meaningful progress, pulling oil prices sharply lower and lifting risk appetite across the board

- March producer price inflation came in well below expectations, supporting the case for cooling underlying price pressure

- Big bank earnings kicked off with broadly strong profit figures, though private credit exposure at some lenders made investors nervous

- Nvidia's launch of AI models for quantum computing sparked a significant rally across the entire quantum sector

The Oil Move That Changed the Day

Brent crude fell 4.6% to $94.79 a barrel on Tuesday. WTI dropped even harder, down 8% to $91.28. To put those numbers in perspective: Brent was trading above $145 on March 9 at the height of the Iran conflict shock. The low $90s hadn't been on the ticker in weeks.

What moved the needle?

Progress, or at least the credible signal of it. Iran's Foreign Minister Abbas Araghchi told his French counterpart that negotiations had advanced on multiple fronts. Trump told reporters that "the right people" in Iran still want a deal. That's still not a ceasefire. But the market has learned to take each of these signals at face value and shave a few dollars off the war premium with every one that lands.

The more structural development was European. France and several other nations are assembling a coalition - without US involvement - to physically reopen the Strait of Hormuz once a ceasefire is in place: minesweepers, naval escorts, the works.

The IEA estimates it would take roughly two months after reopening to bring export volumes back to pre-war levels. Two months. That's the timeline investors are pricing.

The Dow Jones ended 0.65% higher, the Nasdaq gained nearly 2%, its ninth consecutive positive close and the broad market kept pace. Not panic, not euphoria. Just a market that keeps buying each incremental piece of good news and filing the risks away for later.

One Inflation Number That Actually Helped

March producer prices came in sharply below what economists had penciled in.

PPI rose 0.5% month-on-month, against an expectation of 1.1%. The annual figure came in at 4.0%, well below the 4.6% consensus. Core PPI - stripping out food and energy - added just 0.1%.

This followed Friday's CPI print, which told the same story: yes, inflation is elevated, but the energy component is carrying almost all of it. Strip that out and the underlying pressure is actually receding.

The 10-year Treasury yield dropped 5 basis points to 4.25% on Tuesday's data. The euro/dollar rate sat at 1.1792.

The Fed isn't getting relief from the oil price side of the equation, but the non-energy inflation picture is cleaner than it was six months ago. "Higher for longer" hasn't disappeared as a scenario, but Tuesday's data made it look a little less inevitable, and bond markets responded accordingly.

Banks Open the Books: Strength Up Top, Questions Below

The first significant wave of Q1 earnings landed on Tuesday, and the headline numbers were broadly impressive.

JPMorgan Chase (JPM | ▼0.82%) reported record net income of $16.49 billion, a 13% year-on-year increase. EPS came in at $5.94 against a $5.45 estimate. Revenue reached $50.54 billion, clearing the $49.17 billion consensus. Fixed income trading rose 21% to $7.08 billion; investment banking fees surged 28% year-on-year to $2.9 billion. On pure numbers, a strong quarter.

The stock slipped 0.8% anyway. JPMorgan trimmed its full-year 2026 net interest income guidance from $104.5 billion to approximately $103 billion. Markets read forward guidance more carefully than backward-looking results, and a downward revision, however modest, in the most closely-watched revenue line at the world's largest bank has a way of sticking.

CEO Jamie Dimon's tone contributed to the caution. He named what he called "an increasingly complex set of risks", geopolitical tensions, energy price volatility, trade uncertainty, large global fiscal deficits, and elevated asset prices. Dimon is paid to flag these things and usually does so in measured language. He didn't predict a crisis. But he wasn't performing optimism either.

Wells Fargo (WFC | ▼5.70%) had the roughest session. Higher profit on the face of it, but the bank also raised its loan loss provisions, and investors focused on a specific disclosure: approximately $36.2 billion of Wells Fargo's loan book carries exposure to private credit. In a $1 trillion portfolio the ratio isn't alarming, but the number itself was enough to send the stock down nearly 6%.

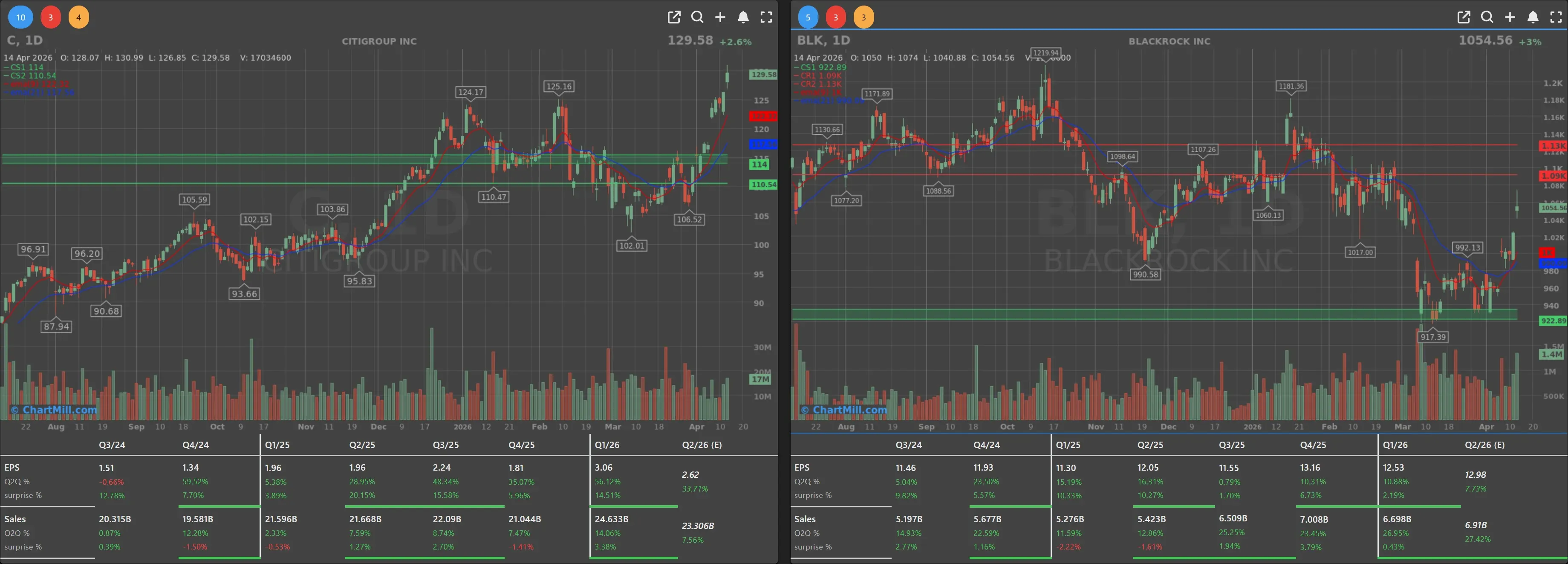

Citigroup (C | ▲2.61%) was the clear bright spot, with better-than-expected results and a meaningful improvement in profitability. The market rewarded it accordingly.

BlackRock (BLK | ▲3.02%), the world's largest asset manager, rounded out the reporting day with Q1 net profit of $2.07 billion, 17% higher year-on-year. Assets under management grew 20% to $13.89 trillion, helped by $130 billion in ETF inflows through iShares and $9 billion into private market strategies. EPS of $12.53 cleared the $11.65 analyst estimate. The stock, down 4% year-to-date before Tuesday, added 3%.

Bank of America and Morgan Stanley report later this week.

Private Credit: The Conversation Banks Had to Have

Wells Fargo's disclosure opened a parallel thread that deserves separate attention.

The $2 trillion private credit market has been a source of quiet unease for months, investor redemptions are picking up, transparency questions haven't resolved, and the exposure of traditional banks as lenders to private credit funds is difficult to quantify consistently. Tuesday brought more numbers onto the table.

Citigroup disclosed $22 billion in loans used to "finance private credit." Wells Fargo's figure was $36.2 billion, though the categorizations weren't perfectly comparable.

The reassurances came quickly: JPMorgan's Dimon said "I don't believe it's a systemic risk." IMF managing director Tobias Adrian told MarketWatch there's no current reason to worry about the banks. Oppenheimer analysts described redemption outflows as "a real but modest headwind."

I take all of that at face value. What I'd flag is that this conversation has a track record of ending with senior figures saying "nothing systemic here" right up until the point where it becomes something.

The 2008 comparison is probably overblown, the leverage mechanics are different, the collateral structures are better understood. But a $2 trillion market where institutional redemptions are accelerating is worth monitoring closely, and Tuesday's disclosures gave the market a concrete reason to do exactly that.

Nvidia Launches Ising and Drags an Entire Sector With It

Nvidia (NVDA | ▲3.80%) launched Ising on Tuesday: the world's first open-source AI model family built specifically for quantum computing.

The name references the Ising model from statistical mechanics, and the two product lines solve concrete problems.

- Ising Calibration reduces quantum processor setup time from days to hours.

- Ising Decoding improves real-time error correction accuracy by up to 3x and speed by 2.5x.

Early adopters include IonQ, Atom Computing, Infleqtion, and Lawrence Berkeley National Laboratory's Advanced Quantum Testbed.

This isn't a consumer product. It's infrastructure-level tooling for anyone trying to build fault-tolerant quantum systems and the market read it as a signal that quantum computing is graduating from science project to something that will eventually need software the same way AI needed CUDA.

IonQ (IONQ | ▲20.16%) gained more than 20%. D-Wave Quantum (QBTS | ▲15.84%) jumped nearly 16%. Rigetti Computing (RGTI | ▲11.50%) added over 11%.

The logic isn't hard to follow: Nvidia is building the software layer for quantum the same way it built the software layer for AI and if quantum turns out to be the next major computing paradigm, controlling calibration and error correction tooling is a strategically critical position. The companies building the actual hardware had every reason to react the way they did.

Amazon Plays Two Different Long Games at Once

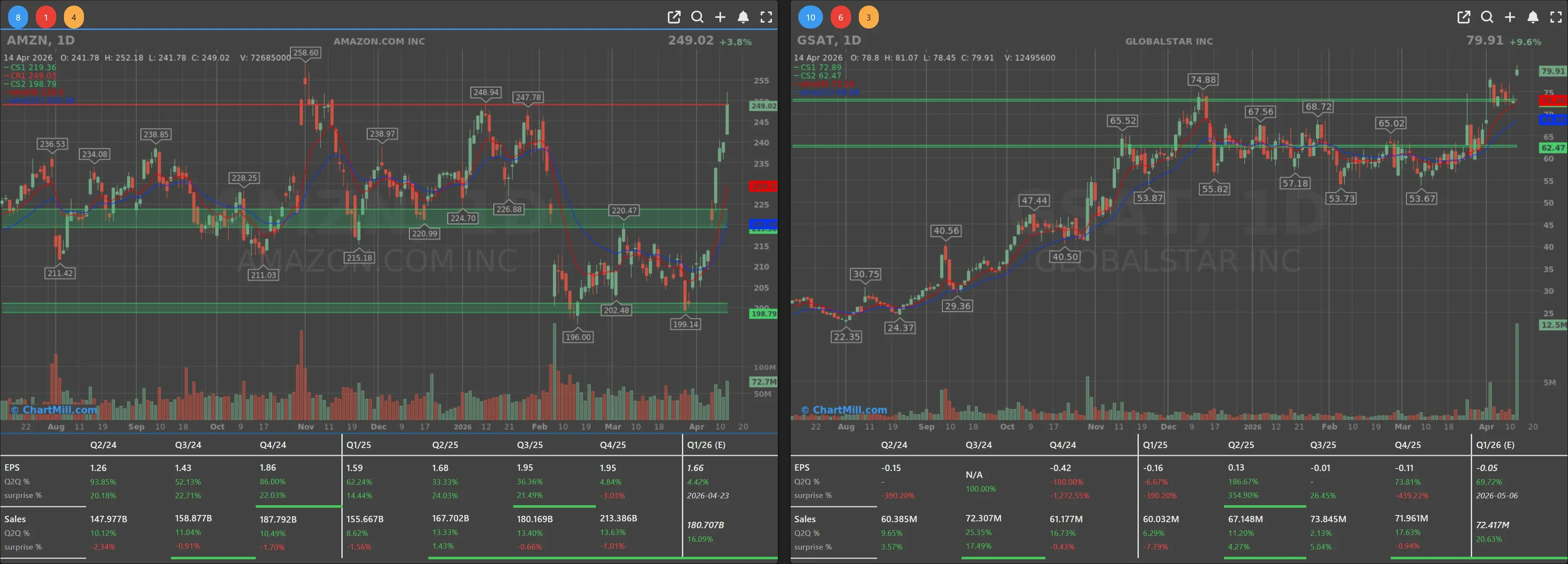

Amazon (AMZN | ▲3.81%) had a busy Tuesday.

First came the Globalstar (GSAT | ▲9.63%) acquisition, $11.57 billion in cash, with shareholders receiving $90 per share or 0.3210 Amazon shares. Globalstar, which Apple already holds a 20% stake in, becomes Amazon's entry into satellite internet.

The direction of travel is obvious: Project 'Amazon Leo' plus Globalstar's existing infrastructure puts Amazon into direct competition with SpaceX's Starlink in a market that is still in the early stages of scaling globally.

The parallel announcement was quieter but arguably more interesting over a longer horizon. AWS launched Amazon Bio Discovery, an AI platform that allows scientists to run complex early-stage drug development workflows without writing code. No splashy promises about curing specific diseases; just a methodical AI application built on top of existing research infrastructure.

Striking, neither of both moves is defensive. Amazon is expanding aggressively into two capital-intensive, technically demanding markets at the same time as its core businesses are running well. That's the posture of a company confident in its earnings floor and actively hunting for the next growth curve.

United Eyes American: A Merger That Would Reshape US Aviation

The story that flew a little under the radar on Tuesday: United Airlines (UAL | ▲2.10%) CEO Scott Kirby reportedly approached the US government about a potential merger with American Airlines (AAL | ▲8.00%).

American Airlines jumped 8% on the speculation alone. A United-American combination would create an airline of extraordinary scale, likely the largest in the world by most measures. Whether a merger of that size clears antitrust scrutiny in the current environment is a genuinely open question.

The history of airline consolidation in the US suggests that deals which look logical from a financial engineering standpoint often run into significant friction when regulators start stress-testing the competitive impact on consumers. Worth watching carefully, but I'd be cautious about treating an 8% gap-up as a done deal.

Elsewhere in the session: Tesla (TSLA | ▲3.34%), Alphabet (GOOGL | ▲3.61%), and Palantir (PLTR | ▲2.52%) all added meaningful ground on the day's broader risk-on tone.

Bottom Line

The S&P 500 is a whisker away from its January record. Oil is falling. Inflation is cooling faster than feared. Banks are printing money even as their CEOs warn about the complexity ahead.

Nvidia keeps widening its technology footprint, and Amazon is spending $11.57 billion as if the growth phase of satellite internet is just getting started.

On paper, Tuesday was constructive from almost every angle. The caveats I keep returning to: "close to a record" and "at a record" aren't the same thing, and this market has had a habit of finding friction right at the top.

Wells Fargo's private credit disclosure, Dimon's pointed risk commentary, and the IEA's warning that oil demand could actually shrink this year are real data points. They don't change the near-term picture materially. But they're worth holding onto the next time the headlines feel uniformly positive.

The record may be coming. It's just not here yet.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.