Finding Quality Compounders with Compounding Quality

By Aldwin Keppens - reviewed by Kristoff De Turck

Last update: Apr 19, 2024

Compounding Quality or @QCompounding used to be a professional investor and now focusses on teaching people about investing. It should not be a surprise the focus is on quality investing.

We first noticed him when he started spreading his wisdom on Twitter (now X). And we were not alone: in about a year he collected over 260K followers and soon received recognition from senior members of the fintwit community. His website compoundingquality.net is a great resource for everything related to quality investing.

ChartMill is a stock screener and also quality investors need screeners! In the rest of the article we will dive into a screen which was created by CQ and you'll also find some Q&A at the end.

What are quality stocks and how can we find them?

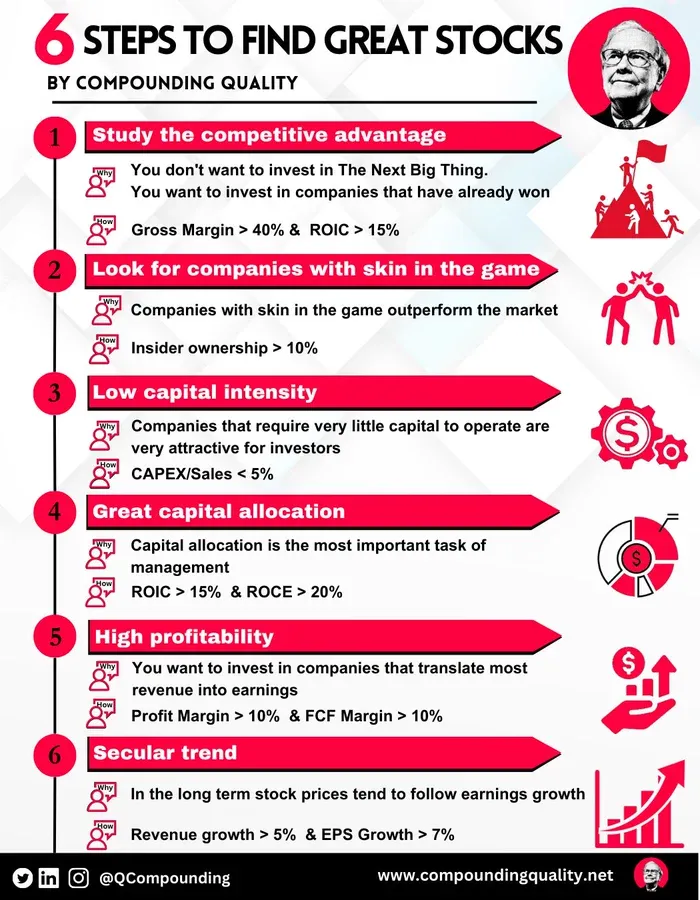

Quality companies have the following characteristics: a wide economic moat, integer management, low capital intensity, good capital allocation, high profitability, attractive historical growth, and a strong secular trend.

As a quality investor you want to invest in the best companies in the world. You don’t want to invest in The Next Big Thing but you want to invest in companies that have already won.

In one of his tweets CQ shared the visual below and this is where we stepped in! ROIC > 15% is a language we understand, so we created the screen in our stock screener and shared it in our library.

You can read a complete article about this screen and the quality investment philosophy on the website of Compounding Quality. The article also gives some examples and alternative filters you can use.

In our implementation, we implemented the rules as shown on the visual.

- For capex/sales, ROCE and ROIC we used the 3 year averages. We believe it makes sense to look at a bit of a longer timeframe to avoid numbers only based on the last twelve months. Feel free to adjust this to 5 year averages or current versions.

- For revenue and EPS growth we used the 5 year CAGR growth numbers.

- We did not include the insider ownership requirement. Not because we don't believe in it, but you can always easily include the condition yourself.

Q&A with Compounding Quality

[ChartMill] The screen we implemented is just a starting point of course. In the next steps we need to analyze and understand the company and check whether all aspects of a quality company apply. But then the valuation part comes into the picture: we do not necessarily need it to be cheap, but we also do not want to overpay (too much?). Can you give us some thoughts about this? Are there things we can check that would quickly reject or confirm the idea?

[CQ] Just like Warren Buffett, I think it’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

However, you can end up with horrible investment results if you overpay for a quality company.

That’s why Compounding Quality’s Investment philosophy can be summarized as follows:

- Buy wonderful companies

- Led by outstanding managers

- Trading at fair valuation levels

[ChartMill] Quality investing is the only true buy and hold method. But this is more theoretically and ideally I assume. So I'm wondering what good reasons would be to sell a stock? An obvious reason seems to be deterioration of fundamentals (for instance because of increased competition or being less dominant in the space). But are there other good reasons? Would you ever sell because a company became overvalued, but all the reasons for owning it are still there? Would you sell to re-allocate to a better opportunity when you are tight on cash?

[CQ] Here are 7 reasons to sell a stock:

- You made a mistake: If you bought the stock for a certain reason and after a while it turns out that you've made an error of judgement, you should consider selling the stock.

- You've found a better opportunity: You should always own the best companies you possibly can which generate the most attractive risk-return characteristics for you as an investor.

- The company is losing its moat: Successful companies must reinvent themselves all the time to keep their competitive advantage.

- The stock is overvalued: This is by far the most dangerous reason to sell a stock. Why? Because great companies always tend to exceed expectations.

- Change in management: When great managers start leaving the company, it might be a reason to sell the stock.

- Growth is slowing down: To generate above-average returns as an investor, you should own companies which are able to grow their earnings at above-average rates.

- Need for cash: If you need cash, it might make sense to sell the least attractive stock you own.

[ChartMill] You mention the "investable universe", a set of around 150 stocks (if I understood correctly) which check all the boxes. How are these companies spread globally? My impression is that it are mostly US companies, followed by some EU companies.

[CQ] That’s exactly correct. Most companies within the investable universe are located in the United States. In general, companies in the US are more profitable and better capital allocators.

[ChartMill] How dynamic is this "investable universe"? Are you often using screeners to find new candidates for your universe? Do you discover new ones often? Are there names dropping off frequently?

[CQ] I am constantly looking for new investment opportunities. That’s why I regularly use screeners to find potentially interesting stocks.

It’s important to highlight that the criteria Compounding Quality uses are very strict. As you already mentioned the investable universe consists of 150 companies. As there are almost 60,000 listed stocks globally, this means that 99,75% of all listed stocks are excluded.

[ChartMill] Any other thoughts you want to share with our users?

[CQ] The best investors in the world are learning machines. Keep an open mindset and keep learning all the time. It’s key to lead a successful life.

In my whole life, I have known no wise people... who didn't read all the time --none, zero. You'd be amazed at how much Warren reads --at how much I read... They think I'm a book with a couple of legs sticking out.” – Charlie Munger