There's something almost surreal about watching markets grind higher while a sitting U.S. president warns he can level an entire country "in one night." Yet that's exactly where we found ourselves on Monday.

The Rundown

- Wall Street closed higher Monday: S&P 500 +0.4% to 6,611, Dow +0.36%, Nasdaq +0.54%

- Iran rejected the ceasefire proposal; Trump's Strait of Hormuz deadline expires 8 PM ET tonight (Tuesday)

- WTI crude above $112/barrel, roughly 20% of global oil supply flows through the Strait

- Friday's jobs report crushed expectations: 178K new jobs added vs. 65K forecast

- Wells Fargo upgrades tech/AI to "favorable," downgrades energy to "unfavorable"

- Strategy (MSTR) buys another 4,871 bitcoin; BTC approaches $70,000

- US inflation data due this week, the next major macro trigger

A Deadline the Market Isn't Fully Pricing In

Monday's session was dominated - as it has been for weeks now - by the Iran-U.S. standoff.

The news flow was whiplash-inducing. Trump told reporters at the White House that talks with Iran were "going well," then turned around and said the ceasefire proposal was "not good enough." He warned that "the whole country could be destroyed in one night, and that night could be tomorrow night," and added that every bridge and power plant in Iran could be taken offline within four hours.

Iran, via mediator Pakistan, rejected the ceasefire outright. Their 10-point response demands a permanent end to the war, reconstruction funding, sanctions relief, and a formal protocol for safe passage through the Strait of Hormuz. Tehran's position is clear: no temporary truce, and certainly no unilateral surrender of Hormuz access.

Despite all of this, the S&P 500 (SPX | ▲0.40%) closed at 6,611, the Dow Jones (DJI | ▲0.36%) added 165 points, and the Nasdaq (COMPX | ▲0.54%) finished at 21,996. Call it cautious optimism. Or call it what it actually is: traders pricing in a last-minute deal rather than a full escalation scenario.

Maybe they're right. But tonight's 8 PM ET deadline is real, and the gap between what Washington wants and what Tehran is offering is not a small one.

Oil told a slightly different story. WTI crude for May delivery rose 0.8% to $112.41/barrel, with Brent for June delivery up 0.7% to $109.77. The Strait of Hormuz accounts for roughly 20% of global oil and gas supply, if that corridor gets disrupted, $112 will look cheap in hindsight. Gold traded nearly flat just below $4,700/troy ounce, while the euro/dollar pair edged up to 1.1543.

Friday's Jobs Report: Much Better Than Expected

Before the geopolitical noise drowns everything out, the March payrolls report from Friday deserves more attention than it's getting.

The U.S. economy added 178,000 jobs last month, nearly three times the 65,000 consensus estimate. Unemployment fell from 4.4% to 4.3%. Wage growth came in at 3.5% year-on-year, moderating slightly from 3.8% in February.

The headline numbers were strong, but there's a footnote worth noting. February's figure was revised sharply lower: from a reported -92,000 to -133,000 jobs. That's a 41,000-job downward revision, which is not nothing. January was revised upward from 126,000 to 160,000, partially offsetting the February miss.

The net read: the labor market is holding up better than feared. The risk of a sudden deterioration is, for now, off the table. That said, federal government employment continued to shrink, which isn't surprising given the ongoing spending cuts. Watch this figure in the months ahead, it's not going away as a headwind.

PMI: Two Indices, Two Stories

There's a contradiction in the March services data worth flagging.

S&P Global's services PMI came in at 49.8, just below the 50-point growth threshold, signaling a marginal contraction and the first sub-50 reading since mid-2023. The composite index dropped to 50.3, the lowest since September 2023.

The ISM services PMI, on the other hand, came in at 54.0, down from 56.1 in February, but still the second-highest reading since October 2024 and solidly in expansion territory. Two surveys of the same sector, pointing in different directions.

I give more weight to ISM for breadth of coverage, but the S&P Global reading is a yellow flag, not a green one. One month doesn't make a trend, but two in a row would.

Manufacturing held up better: S&P Global's manufacturing PMI improved from 51.6 to 52.3 in March.

Wells Fargo Repositions: Tech In, Energy Out

Wells Fargo made a notable sector call on Monday.

They upgraded the tech sector from "neutral" to "favorable," pointing to double-digit earnings growth in Q4, relatively low debt compared to the S&P 500 average, and AI-driven profit growth running above the market average in 2026. Their key argument on valuation: the recent tech sell-off has made entry points more attractive.

Alphabet (GOOGL | ▲1.43%) and Amazon (AMZN | ▲1.44%) both bounced around 1.4%. Neither is back at its highs, but the worst of the AI-sector correction may be behind us, at least that's what Wells Fargo is betting.

I think they have a point on valuations, though the geopolitical backdrop adds a layer of uncertainty that no upgrade fully accounts for.

On the flip side, Wells Fargo downgraded energy from "neutral" to "unfavorable," arguing that the recent energy rally is an opportunity to take profits, not add exposure. Their read on earnings prospects for energy companies: weak. The price action on Monday backed that up.

Despite higher oil, Chevron (CVX | ▼0.06%) and Occidental Petroleum (OXY | ▼0.02%) barely moved. The equity market is not buying the oil story at these levels and that's a meaningful signal.

Company News

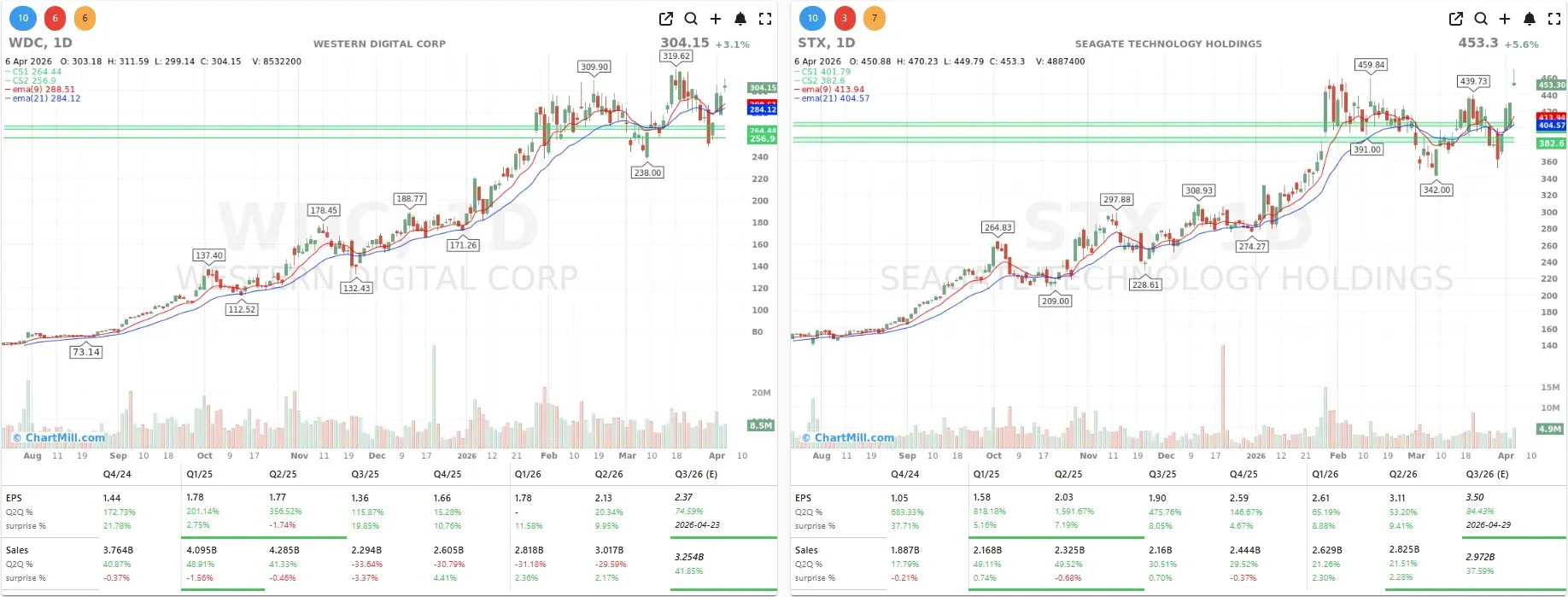

Seagate and Western Digital had a good Monday.

Morgan Stanley reiterated its Overweight rating on both names, and elevated Seagate (STX | ▲5.58%) to "top pick" status in the storage sector. Western Digital (WDC | ▲3.11%) followed along. Storage tends to fly under the radar, but both setups look interesting on the back of a conviction call from a major bank.

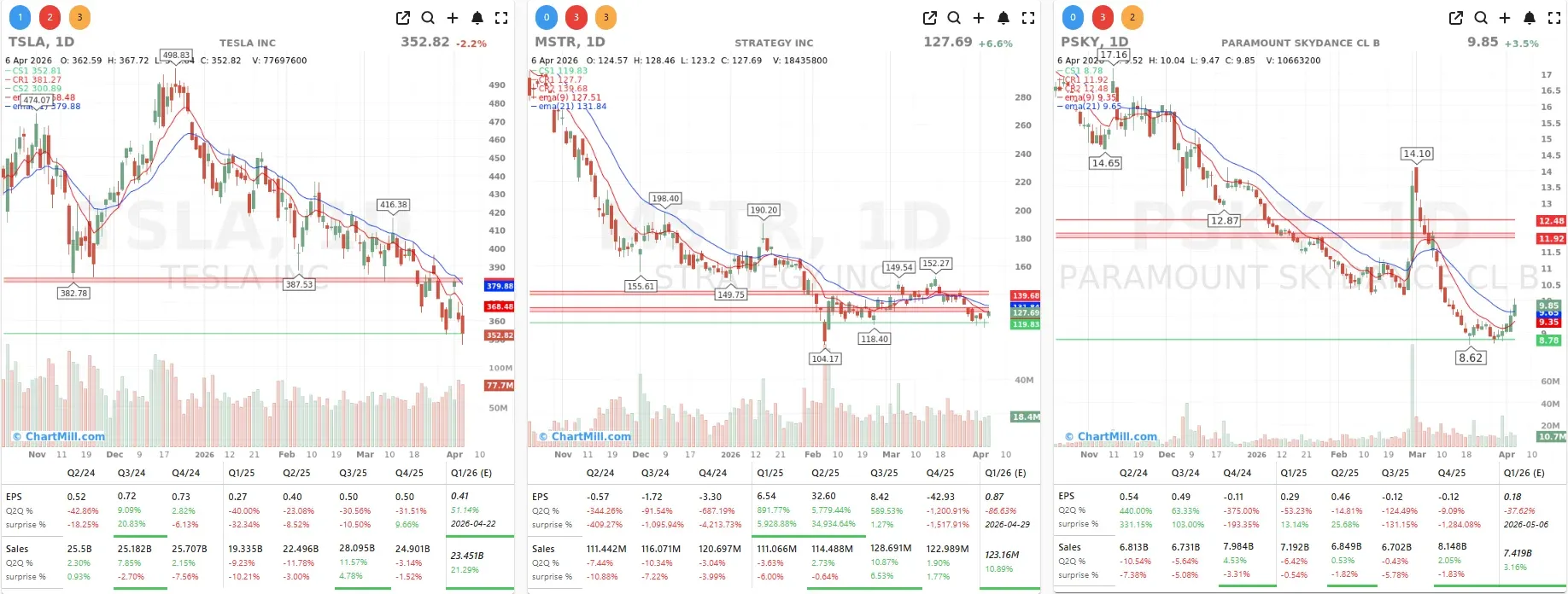

Tesla (TSLA | ▼2.15%) added to Thursday's 5.4% drop following disappointing delivery figures. The stock has been grinding lower for weeks, and nothing in Monday's session changed that narrative.

Strategy (MSTR | ▲6.56%) climbed on bitcoin's move and disclosed it had purchased another 4,871 BTC over the past week. Bitcoin itself rose 3.5%, approaching the $70,000 level. At this point, Strategy's ongoing BTC accumulation is less news and more background noise, but the stock keeps responding to it.

Paramount Skydance (PSKY | ▲3.47%) was reportedly in discussions with three Gulf state sovereign wealth funds about a roughly $24 billion participation to support its planned acquisition of Warner Bros. Discovery, according to the Wall Street Journal. If that capital comes through, it's a significant vote of confidence from investors who tend to think in decades, not quarters.

In M&A, Neurocrine Biosciences (NBIX | ▲0.67%) announced it's acquiring Soleno Therapeutics(SLNO | ▲32.31%) for $2.9 billion, or $53 per share, to expand its endocrinology and rare disease portfolio. Soleno closed at $52.25, the market is basically pricing this deal as done.

What's on the Radar

Tonight's Iran deadline is the single biggest variable in the room right now. Everything else, the jobs beat, the PMI readings, the sector rotations, matters significantly less if the Strait of Hormuz becomes an active flashpoint. The bond market is calm, but that can change quickly.

Beyond geopolitics, U.S. inflation data is due this week. With a strong labor market and oil prices north of $110, a hot print would put the Fed in a genuinely uncomfortable position.

Bottom line: I'm watching Iran closely tonight. Until the deadline passes, keeping some dry powder available makes more sense than chasing the rally.

ChartMill Market Desk - Kristoff

This daily update is prepared by ChartMill for informational purposes only and does not constitute investment advice. Always do your own due diligence before making investment decisions.

Next to read: Market Breadth Improves Further as Short-Term Participation Broadens